We've been doing a lot of updates for you when it comes to the changes on flood insurance rates per state and per city in those states. In those blogs, we've mentioned a lot about what stays and what changes in federal flood insurance once the new program kicks in.

Today, we'll do a deep dive on these changes with the National Flood Insurance Program (NFIP) policies itself, how it works, how you will be rated, and understanding how flood insurance will work with the new Risk Rating 2.0.

We want to talk about the specifics of how Risk Rating 2.0 or NFIP 2.0 will impact the coverages in flood insurance for both residential and commercial policies. So how will flood insurance coverage change with the new Risk Rating 2.0 program?

Risk Rating 2.0

First, let's discuss what this new program is all about. The Risk Rating 2.0 is a new setup for federal flood insurance under the Federal Emergency Management Agency (FEMA) that aims to provide policyholders across the United State a rating structure that eliminates any rating disparities and get people more accurate flood insurance rates with the National Flood Insurance Program (NFIP).

This new program is equity in action and will consider a lot of old and new rating factors when it comes to flood insurance. These factors and conditions are the things that the Risk Rating 2.0 will consider and can also help you determine if you're going to get a premium increase or rate increase just by looking at your property details. We'll talk more on the specifics in our future blogs on this, but to give a brief preview here are the things that impact your rate which will stay with the Risk Rating 2.0:

- Flood zone designation based on community flood maps.

- Distance of the property to a body of water.

- Prior flood insurance claims or history of flood claims made with the property

- Policy assumption and policy transfer.

- The grandfather rule.

- Pre-FIRM subsidies or Pre-Flood Insurance Rate Map discounts.

The new things that will also impact your rates. These things are more focused on individual properties, so there's a fingerprint of flood risk when it comes to the Risk Rating 2.0. This is to say that your rate won't be the same as your neighbors:

- Types of flooding that your property experience.

- Flood frequency impacting the community and your property.

- First-floor height or distance of the first livable area to grade (ground).

- Elevation of the structure or the property itself.

- Flood Risk Mitigation Measures made on the property.

Again, we'll talk more about these in future episodes, but for now, we want to focus on the impact on flood coverage so that property owners and insurance agents alike can get an understanding of this. One step at a time.

Flood Insurance Coverage 2.0

Now, we get to the hot stuff, what changes when it comes to flood insurance coverage with the National Flood Insurance Program under the Risk Rating 2.0?

Well, I have to break it to you, but so far nothing changes. Which doesn't mean that they won't change in the future. There's a lot of things coming into play when it comes to coverage amount or limits — I mean we're still going through a pandemic.

Generally, this means that residential and commercial properties will still get that coverage for flood damage on dwelling and contents. By dwelling, this means the insured building or your house itself whereas contents will be the things that are inside the dwelling. Let's get down to specifics for everyone's awareness.

Dwelling coverage from FEMA and the National Flood Insurance Program (NFIP) will cover the flood damage to the construction impacted by the flood like walls, ceilings, roofs, fences, floor surfaces, water heaters, furnaces, air-conditioning systems. This coverage will also include everything that goes into the cleanup and debris removal. The coverage for dwelling on residential properties is maxed at $250,000 however for commercial properties, this coverage is $500,000 maximum.

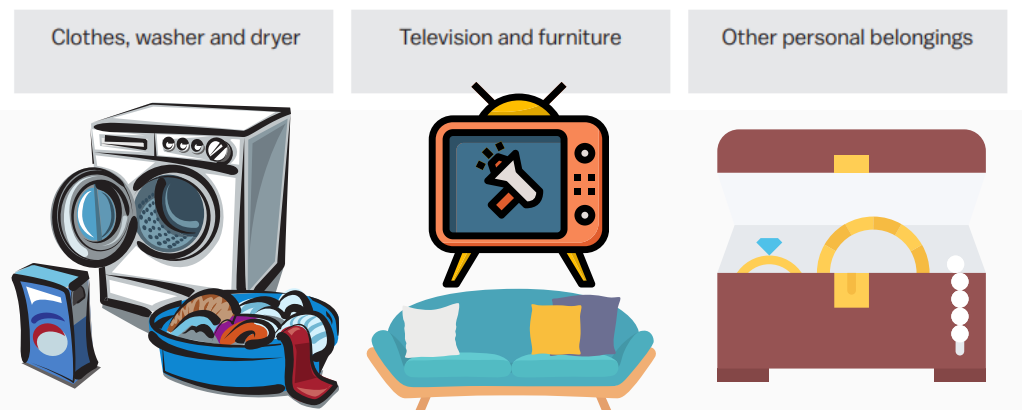

Contents coverage on the other hand is more concerned with the personal property you have within the insured dwelling or building. This means that you will get covered for a maximum amount of $100,000 for clothes, washers, dryers, television, furniture, and other personal belongings that were impacted by flood damage. This amount will be the same regardless if you're carrying a commercial or residential policy.

What's important to note about coverage is that there's still the Increased Cost of Compliance (ICC) which can make you legible for additional flood insurance coverage the NFIP. Quick disclaimer, you and your community will have to apply for this one in order to make sure that you're legible to get it. So what's this coverage you ask?

Increased Cost of Compliance

One of the things that won't change with the NFIP as the Risk Rating 2.0 kicks is the ICC or Increased Cost of Compliance. This coverage is something we can call additional since this is mostly provided at $30,000 maximum for policyholders and is intended to ensure that you will reduce the impact, if not the overall risk of flooding on the listed property. Generally, this involves flood mitigation efforts such as the installation of flood openings and the labor that goes into making that happen.

When Will Risk Rating 2.0 Happen?

It's important to know this information before you move into federal flood insurance or move to the private market. This new Risk Rating 2.0 program will change flood insurance policies across the United States starting this October 1st, 2021 for new business or new policyholders.

On the other hand, if you're going to have a renewal, you can choose to not adapt until April 1st, 2022 since this is the date the FEMA aims to have the new program take full effect on all flood insurance policyholders.

For now, we wait for updates with the coverages, but this is just one of the things that really won't change with the Risk Rating 2.0. If you have any questions on coverages in flood insurance, your flood risk fingerprint, or anything at all about floods and flood insurance, reach out to us by clicking below.

Remember, we have an educational background in flood mitigation which lets us help you understand flood risks, your flood insurance, and mitigating your property long-term.

{kind=link}