The Federal Emergency Management Agency (FEMA) is rolling out changes when it comes to flood insurance rates across all states in the country. Today, we will unpack these changes coming to Massachusetts and how they can impact your flood insurance in the future.

The State of Massachusetts is one of the most beautiful places where you can get a good time from the coasts. However, when it comes to floods, the coast might be the biggest threat to residents across the state. As we dive deeper into the hurricane season, we'll face that constant threat of coastal floods across the state. When talking about flood risk, this season might be the biggest one since it can bring different types of floods throughout the state.

Every year, everywhere in the country there are floods happening. This may be due to spring runoff, water being redirected away from their natural channels, flash floods, storm surges, and more. This is why it's important to have the right flood coverage for your property and make sure that you minimize the risk of flood damage, if not eliminate it entirely.

Today, we want to discuss your federal flood insurance changes with the National Flood Insurance Program (NFIP) as they wind up to roll out the Risk Rating 2.0. We want to talk about the good, the bad, the ugly changes coming to flood insurance rates, and what it can mean for flood insurance for the Bay State.

These changes are expected to take effect on October 1st, 2021.

The NFIP 2.0

The Risk Rating 2.0, or commonly known as NFIP 2.0 as well, is more of a move of equity. This update on the federal flood insurance program itself will allow you to no longer pay more than your fair share when it comes to premiums as this would now be based on the value of your property or home starting this October.

Other than the property values, there are other things that take place when FEMA and the National Flood Insurance Program are assessing the flood insurance rates you'll see with the new flood insurance rating structure. You want to consider other important things like:

- History of flooding and flood damage

- The overall risk of flooding in the area and flood frequency

- History of flood insurance claim and flood claims frequency

- Flood maps designation of the residential property or commercial building

- Property flood mitigations and relation to the base flood elevation in the state

When it comes to the rate changes happening across the country, you're going to see these colors in ranges which represent these changes with flood insurance rates from FEMA. Now, each of these colors represents the good, the bad, and the ugly changes coming to each state.

t's important to remember that the National Flood Insurance Program will provide you that $250,000 flood insurance coverage on building damage and $100,000 in damage to contents however you're going to have to offset your schedule if you want to get insured right now. The National Flood Insurance Program will still have to follow that 30-day waiting period before the policy can take effect on the property.

The Good

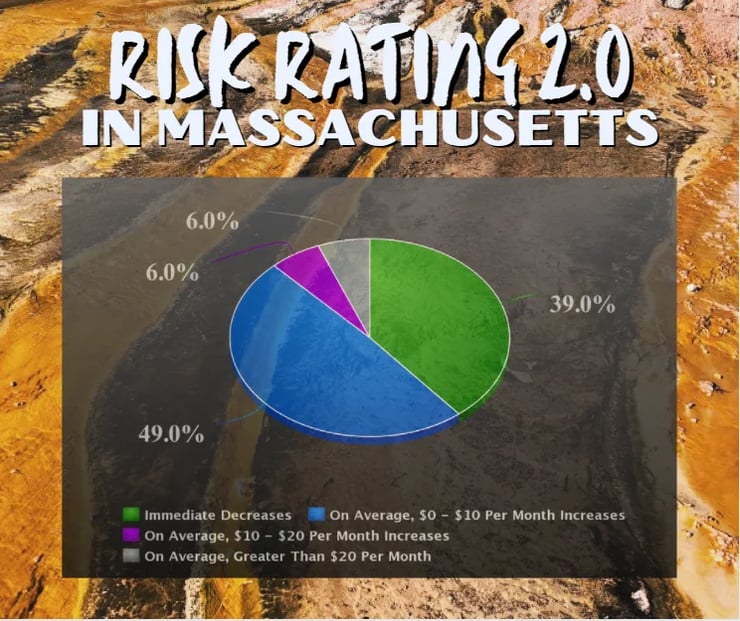

First, let's start with the good change coming to the state of Massachusetts which we'll show as the green slice. This will impact 39% or 22,599 of the active policies that FEMA has in the state.

We call this a good change since it will cause an immediate decrease of more than $100 ($1200 per year) for FEMA policyholders, and when you're in coastal areas like Massachusetts this can really help with that expensive federal flood insurance. Equally, coastal areas like this also face the threat of having the private market pull away from providing flood insurance once the risk becomes too high for them.

This can be very good for those who can't get a policy from the private flood insurance industry. It's important to remember that despite having a shorter waiting period and limitless flood coverage, private companies have the option to stop providing flood policies for high-risk areas and non-renew policies after filing a flood claim.

The Bad

Now, let's move over to the things you need to watch out for with the upcoming NFIP 2.0. Starting with the blue slice, which we also call the bad change. This will be bringing an increase to flood insurance rates to policyholders.

About 49% or 28,787 policies will be impacted by this change. The increase in rates ranges from $0 to $10 per month ($0 - $120 per year). If you look at the current average of $1500 on federal flood insurance in the state, this change can really mean a lot and even harder to swallow for those moving into flood zones where flood insurance will be required.

The Ugly

When it comes to the ugly changes, you're going to have to look at the last two slices on this pie: the pink and grey slices. Although both will bring an increase to rates in Massachusetts policyholders, it's important to highlight here that one will be the uglier change.

The pink slice will cover about 6% or 3,413 of active policies. This will get the affected properties an increase in flood insurance rates ranging from $10 to $20 per month ($120 - $240 per year).

On the other hand, the grey slice is going to impact the remaining 6% or 3,712 policies in the state with an increase in rates of more than $20 per month (>$240 per year). This means that some property owners may have to deal with a $100 increase when the Risk Rating 2.0 kicks in.

The premium increases and rate increases can be very difficult to manage for high-valued homes. No one would want to pay thousands of dollars only to get covered for $250,000 on their $500,000 home. This is why it's important to also connect with a flood specialist on how to get through the private insurance industry.

You can see the full graph of these changes below:

When Will It Happen?

Now, the date when you can adopt this program really depends if you're doing a renewal or if it's a new business policy. You see, you can expect these changes to start on October 1st and you're going to adapt to these rate changes if you're buying flood insurance from FEMA on or after that date.

On the other hand, if you're doing a renewal with FEMA after that date then you don't have to take in these new rate changes until April 1st, 2022.

So, you want to be very ready for this. We've been talking about this since last year since basically the NFIP is already 30 years old already and is in need of this change.

If you have questions on these upcoming changes, what are your flood insurance options in Massachusetts, or anything about flood, reach out to us through the links below. You can also watch this on our YouTube channel.

Remember, we have an educational background in flood mitigation and we want to help you understand flood risks through education and awareness in flood insurance and preparedness.

{kind=link}