.jpeg?width=290&height=174&name=download%20(9).jpeg)

In this podcast we are discussing the 5 ways to verify a flood zone. Verifying a flood zone by one way can be dangerous exposing you and property owners. So what are the ways to verify a flood zone? Each way is listed below

- Flood Insurance Rate Map

- FEMA Map Service

- Letter of Map Amendments and Revisions

- Special Flood Hazard Determination Form

- Elevation Certificates

Flood Insurance Rate Maps

.jpeg?width=430&name=download%20(9).jpeg)

Let's discuss the first way to verify a flood zone, which is a flood insurance rate map. So what is a flood insurance rate map?

A flood insurance rate map also called a (FIRM) is a product of the Flood Insurance Study (FIS) for a community and is available in paper form and digital form. It's an official map of a community within the United States that displays the floodplains, more explicitly special hazard areas and risk premium zones, as delineated by the Federal Emergency Management Agency.

According to FEMA a firm should show four things

- Roads and map land marks,

- A community's base flood elevations,

- Flood zones, and

- Floodplain boundaries.

So where can a FIRM be found?

The FIRM for a community, and the local floodplain management regulations, should be on file and available for viewing at the office of the community floodplain administrator.

FEMA Map Service

The FEMA Flood Map Service Center (MSC) is the official public source for flood hazard information produced in support of the National Flood Insurance Program (NFIP).

This tool can be used to access your local flood maps, access a range of other flood hazard products, and take advantage of tools for better understanding flood risk.

The FEMA Map Service Center stores some very important information for property owners. It stores any changes to the Firm like

- Revisions

- Amendments

- Revalidation

So that brings us to the 3rd way to verify a flood zone which is Letter of Map Amendments and Revisions

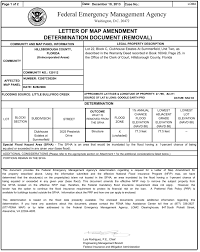

Letter of Map Amendments and Revisions

The 3rd way to verify a flood zone is by checking the Letter of Amendment or Revision.

Let's first of all understand the difference between amendments and revisions. A Letter of Map Amendment (LOMA) is an official amendment, by letter, to an effective National Flood Insurance Program (NFIP) map. A LOMA establishes a property''s location in relation to the Special Flood Hazard Area (SFHA). LOMAs are usually issued because a property has been inadvertently mapped as being in the floodplain, but is actually on natural high ground above the base flood elevation.

Now that we know what know what a letter of map amendment is let's get an understanding of map revisions.

A Letter of Map Revision is FEMA's modification to an effective Flood Insurance Rate Map (FIRM), or Flood Boundary and Floodway Map (FBFM), or both. LOMRs are generally based on the implementation of physical measures that affect the hydrologic or hydraulic characteristics of a flooding source and thus result in the modification of the existing regulatory floodway, the effective Base Flood Elevations (BFEs), or the Special Flood Hazard Area (SFHA). The LOMR officially revises the Flood Insurance Rate Map (FIRM) or Flood Boundary and Floodway Map (FBFM), and sometimes the Flood Insurance Study (FIS) report, and when appropriate, includes a description of the modifications.

We all know that FEMA sometimes is not the best at simplifying things so to get an easy understanding of the difference between amendments and revisions. An amendment generally has to do with a particular property while a revision is a modification of the actual flood map.

Like mentioned earlier these amendments and revisions can be found on the FEMA Map Service site. Since these are public records they are always kept on file at the local level and on the flood map plan.

A revalidation is when the LOMA or LOMR has been confirmed after a FIRM has changed. Now not all LOMA's will be confirmed after a FIRM change. Just recently we had a customer that not only was not revalidated but had their base flood elevation increase by 7 feet significantly increasing their flood insurance rates. Even FEMA says that they try to do the best they can to revalidate things but sometimes properties are missed.

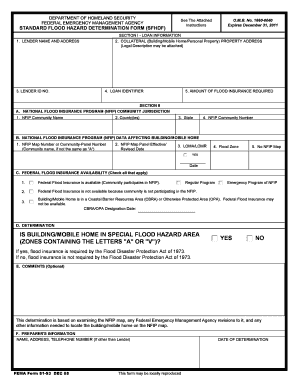

Special Flood Hazard Determination Form

The 4th way to verify a flood zone is through a special flood hazard determination form. There is a picture of one below.

Now while these forms can be very beneficial they can also be dangerous as many times they are done by 3rd party vendors. Mortgage companies, real estate companies, title companies, and insurance companies all use these forms for flood zone verification.

The problem in using this form is when dealing with 3rd party vendors they may have different information. It's not usual for a mortgage company to have a different flood zone on this form from what an insurance company has on the form.

FEMA recommends using this form with something like the FEMA Map Service to make sure you have the correct zone.

So what happens if there are two different zones? The higher zone has to be used until something like an elevation certificate can prove otherwise.

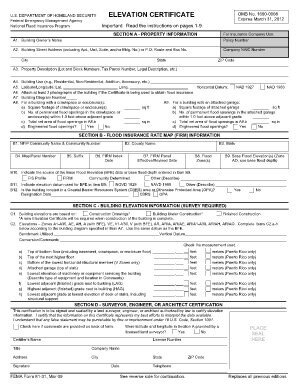

Elevation Certificates

The last way to verify a flood zone that we are going to discuss are elevation certificates.

So what is an elevation certificate?

An elevation certificate is an important tool that documents your building’s elevation. It compares it to the base flood elevation when there is one. There are several parts of an elevation certificate that are important.

- The flood zone

- Base flood elevation

- Building diagram type

- Lowest adjacent grade of the property

- Lowest floor of servicing equipment

- Lowest rated floor

The picture below shows where the flood zone is located on an elevation certificate. It also shows where the building diagram type is located as well as the base flood elevation, and elevations of the servicing equipment and lowest adjacent grade.

Using an elevation certificate to verify a flood zone by its self can be dangerous. If the FIRM has changed since the elevation certificate has been done then the flood zone on the certificate could actually be wrong. It is important to look at the date the elevation certificate was completed and compare it to the FIRM date.

It's also important to remember that if the lowest adjacent grade on the elevation certificate is above the base flood elevation then the property could be a candidate for LOMA which could change the flood zone.

FIRMS, FEMA Map Service, Letter of Map Amendments and Revisions, Special Flood Hazard Determination Forms, and Elevation Certificates are all great tools for verifying flood zones. It can be dangerous using any of them alone to verify the flood zone. Its always recommended that at least 2 of these tools are used together. At The Flood Insurance Guru we recommend using FEMA Map Service with any of these tools.

If you have questions about using any of these tools, your current flood zone, or even getting your flood zone changed then make sure to visit our website Flood Insurance Guru. You can also visit our YouTube channel or Facebook page where we do daily flood education videos.

{kind=link}