Why Flood Zone Classification Matters

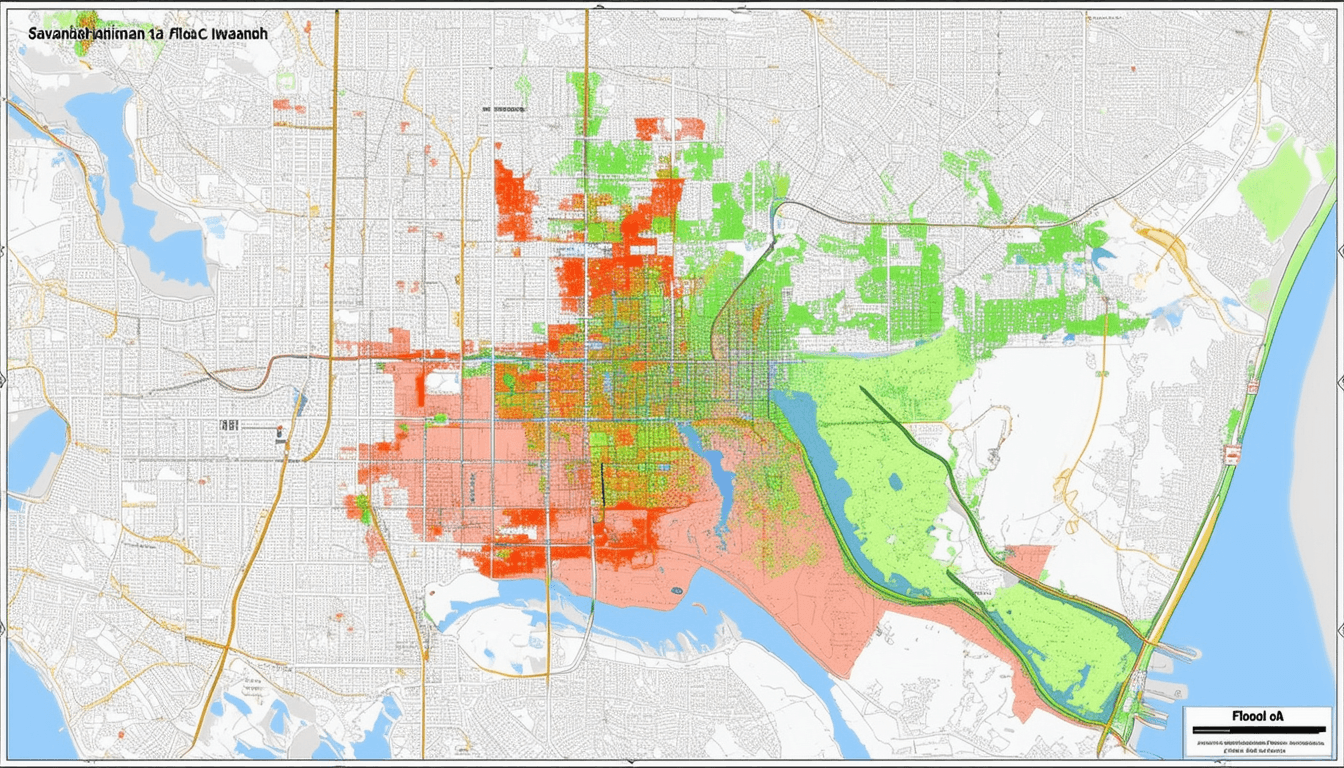

Understanding your flood zone is critical. This knowledge influences everything from insurance needs to emergency planning. The Federal Emergency Management Agency (FEMA) maintains flood maps that categorize each property’s flood risk level. Here’s a quick breakdown of Georgia’s flood zone classifications:

| Flood Zone | Description | Insurance Requirement |

|---|---|---|

| High-Risk Areas (A Zone) | 1 in 4 chance of flooding over a 30-year mortgage period | Mandatory flood insurance |

| Coastal Areas (V Zone) | Areas at high risk with wave action | Mandatory flood insurance with additional considerations |

| Moderate-Risk (X Zone) | Lower but still possible risk | Flood insurance optional, highly recommended |

| Minimal-Risk Areas | Outside the 100-year floodplain, low risk | Flood insurance optional, encouraged for added security |

Homeowners in high-risk zones like along the Chattahoochee river or ogeechee river are often required to have flood insurance as a condition of their mortgage, especially if backed by federally regulated lenders like Freddie Mac or Fannie Mae. Understanding this designation helps you ensure compliance and avoid costly penalties.

Why Flood Zone Classification Matters

Understanding your flood zone is critical. This knowledge influences everything from insurance needs to emergency planning. The Federal Emergency Management Agency (FEMA) maintains flood maps that categorize each property’s flood risk level. Here’s a quick breakdown of Georgia’s flood zone classifications:

| Flood Zone | Description | Insurance Requirement |

|---|---|---|

| High-Risk Areas (A Zone) | 1 in 4 chance of flooding over a 30-year mortgage period | Mandatory flood insurance |

| Coastal Areas (V Zone) | Areas at high risk with wave action | Mandatory flood insurance with additional considerations |

| Moderate-Risk (X Zone) | Lower but still possible risk | Flood insurance optional, highly recommended |

| Minimal-Risk Areas | Outside the 100-year floodplain, low risk | Flood insurance optional, encouraged for added security |

Homeowners in high-risk zones like along the Chattahoochee or Ogeechee rivers are often required to have flood insurance as a condition of their mortgage, especially if the mortgage is backed by federally regulated lenders like Freddie Mac or Fannie Mae. Understanding this designation helps ensure compliance and avoid costly penalties.

Strategies to Reduce Flood Insurance Costs

There are effective ways to potentially lower your flood insurance costs, even if you live in a high-risk zone:

-

Elevate Your Home: Raising your home above the Base Flood Elevation (BFE) can lead to significant savings on premiums and reduce the risk of flood damage.

-

Invest in Flood-Resistant Features: Installing flood vents, sump pumps, or barriers can mitigate flood risks and, in some cases, lower your insurance costs.

-

Consider Partial or Supplemental Coverage: For lower-risk areas, consider adding flood endorsements to your homeowner’s policy or opting for a deductible plan that balances protection with premium affordability.

-

Shop Around: Don’t assume one flood insurance provider is your only option. Compare both NFIP and private insurers to find coverage that fits your needs and budget.

Staying Updated on Flood Risks and Regulations

Georgia’s flood zone maps are regularly updated to reflect changes in climate, rainfall patterns, and urban development. Staying informed helps you remain compliant and ensures your insurance policy aligns with the latest flood risk assessments. Here’s how to keep up-to-date:

- Check FEMA and State Updates Regularly: FEMA revises flood maps periodically. It’s important to review these updates to confirm your zone designation, as changes can affect your insurance requirements.

- Engage with Community Resources: Participate in local meetings or online forums focused on flood risk, emergency preparedness, and insurance regulations to stay connected with evolving state guidelines.

- Consult Experts Annually: Schedule an annual consultation with your insurance provider or a floodplain expert to review your coverage and make adjustments based on any recent changes in your zone or flood risk.

In Summary: Protect Your Home Against Flood Risks

Understanding and navigating state-mandated flood coverage areas in Georgia enables you to take the necessary steps to safeguard your home and financial well-being. With the right information, insurance, and proactive measures, you can face flood risks with confidence, knowing you’ve done everything possible to protect your property. By staying informed and making strategic decisions today, you ensure a more secure future against the unpredictable nature of flooding.