Did your mortgage payment suddenly jump by $200 to $300 a month without warning?

You are not imagining it. This issue is hitting homeowners across Birmingham, especially in flood-prone ZIP codes like 35211, 35124, and areas near Valley Creek. The cause is not your loan rate, and it is not a mistake. It is a breakdown inside your escrow account that most lenders never explain clearly.

In this article, you will learn why your mortgage payment spiked so sharply, how flood insurance triggered the increase, and exactly how to correct it quickly, even if your lender says nothing can be done.

What Really Caused Your Escrow Shortage

Your higher payment is not just about this year. You are paying for last year too.

Mortgage servicers use escrow accounts to pay your property taxes and insurance. When an insurance bill increases, most banks do not adjust your payment immediately. They quietly cover the difference and wait until the next scheduled escrow review, which can be six to eight months later.

Here is a common Birmingham timeline:

-

Last year your FEMA flood insurance increased from $800 to $1,400

-

Your bank paid the higher bill without notifying you

-

You continued making the old mortgage payment

-

Months later the escrow review reveals a shortage of $600 or more

At that point, the bank raises your payment to recover what they already paid.

Why the Payment Increase Feels So Extreme

When your escrow is reviewed, the lender does three things at once:

-

Recovers the shortage from last year

-

Funds the higher insurance cost for the coming year

-

Adds an escrow cushion, usually two months of expenses

This is why a $600 annual insurance increase can translate into a $2,000 to $2,500 jump spread across your next twelve payments. It feels sudden because it is correcting months of delayed accounting.

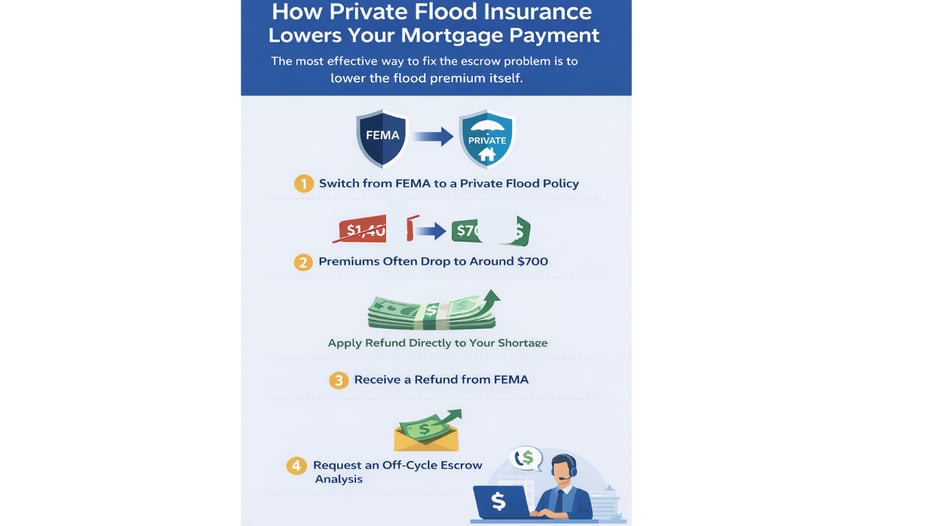

The Fastest Fix: Request an Off-Cycle Escrow Analysis

You do not have to wait for the bank’s schedule. You can take control.

If your insurance changed or you suspect an increase, call your mortgage servicer and say this exact phrase:

"I need to request an off-cycle escrow analysis."

This forces the bank to recalculate your payment immediately, not at the next annual review.

Why Timing Matters

Requesting this early, especially in January or soon after switching policies:

-

Stops the escrow hole from growing

-

Applies savings immediately

-

Lowers your monthly payment faster

This single step often saves homeowners thousands over the course of a year.

Frequently Asked Questions (FAQ)

Why did my mortgage go up when my flood insurance only increased by $500?

Because your lender is recovering the shortage, funding the new rate, and adding a reserve cushion at the same time.

Can I request an escrow analysis whenever I want?

Yes. You can request an off-cycle escrow analysis at any time.

Is private flood insurance really cheaper than FEMA?

In many Birmingham ZIP codes, yes. Savings of 30 to 50 percent are common.

Will my mortgage drop automatically after switching flood insurance?

No. You must request an escrow recalculation or the savings will not apply until the next annual review.

Take Control Before the Next Increase Hits

Birmingham homeowners do not have to accept rising payments as inevitable. By switching to private flood insurance and forcing an off-cycle escrow analysis, you can regain control of your mortgage and your budget.

If your payment has already jumped or you want to prevent the next increase, now is the time to act. Let us help you stop the escrow cycle and bring your mortgage back to a manageable level.

{kind=link}