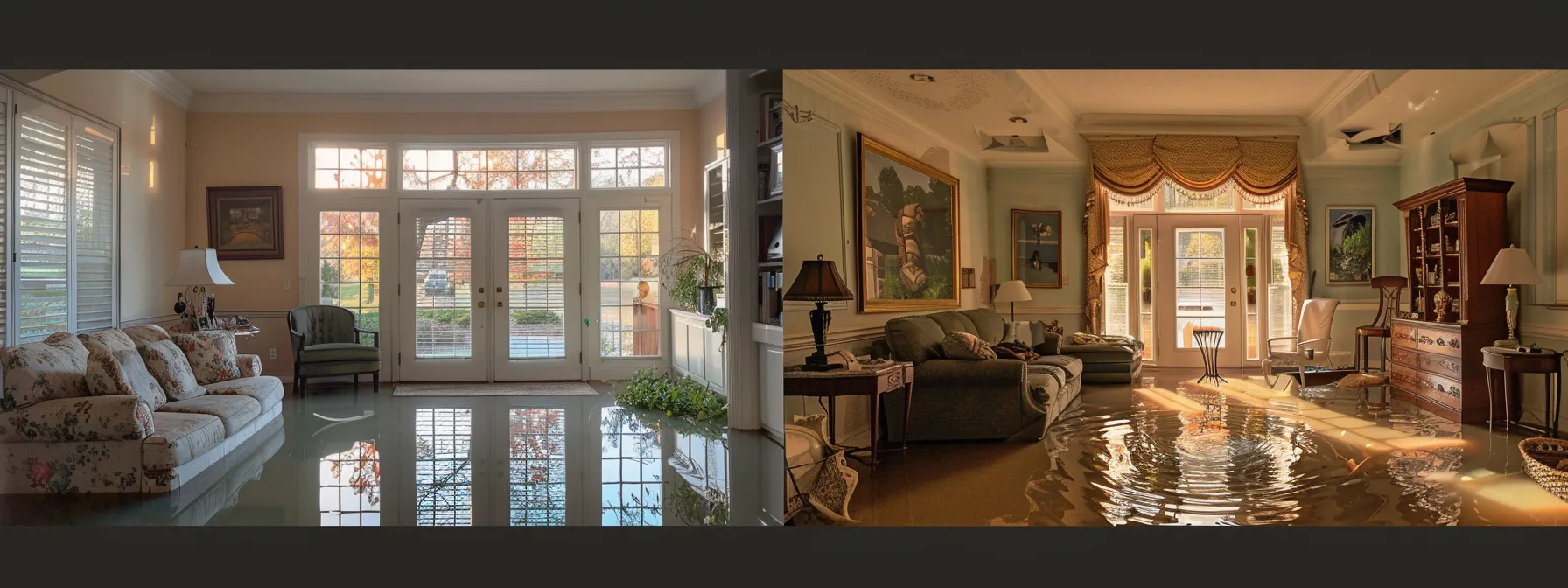

If you own property in Georgia's AE flood zone, you're likely acquainted with the unique challenges presented by the risk of flooding. Securing an appropriate flood insurance policy isn’t merely advisable; it's often a requisite.

The cost of this insurance hinges on various factors, from the intricacies of your property's location to the specifications laid out in the National Flood Insurance Program (NFIP). To assist you in navigating the intricacies of flood insurance and to help you make informed decisions that protect your assets, we'll provide you with a clearer understanding of what dictates rates in high-risk zones.

Keep reading to uncover actionable insights and tips to mitigate the financial impact of flood risk on your Georgia home.

BREAKING DOWN FLOOD INSURANCE COSTS IN GEORGIA'S AE ZONE

If you own a home in Georgia's AE Zone, a high-risk flood area designated by the Federal Emergency Management Agency (FEMA), you may have questions about your insurance needs and costs.

Flood insurance is separate from typical home insurance, and often a mandatory addition to your mortgage in these zones. Understanding the complexities of the National Flood Insurance Program (NFIP) and other factors influencing insurance costs in AE Zones is critical.

While premiums can vary widely, knowing the average cost range helps set expectations. Additionally, an appraisal of your property's unique risks ensures you're not caught off guard. Let's walk through the essential steps to obtain an accurate insurance quote, keeping your investment safeguarded against potential floods. Georgia flood insurance

Identifying AE Zone Characteristics in Georgia

As you step into the task of evaluating your home's flood insurance needs in Georgia's AE Zone, you must first understand the unique characteristics that define this area. AE Zones are recognized as high-risk floodplains where water levels could rise rapidly during a significant storm event, prompting a swift response from emergency management services. Acknowledging this risk is the starting point for grasping the potential cost implications for your insurance policy.

Deciphering the flood risk tied to your Georgia property involves consulting updated flood maps. These maps, created by FEMA, indicate the severity and frequency of flooding, a crucial factor for insurers when determining your premium. Familiarizing yourself with the AE Zone designations on these maps not only enlightens you about the floodplain dynamics but also prepares you to make informed decisions about the cost of safeguarding your home against water damage.

Factors Influencing Insurance Costs in AE Zones

Your home's elevation relative to the nearest Base Flood Elevation (BFE) heavily influences your flood insurance premiums. Policies may range in cost, reflecting the level of risk assessed: homes at or above the BFE in Georgia will generally attract lower rates, while those below it can expect higher premiums. Knowing your home's specific elevation can be as critical as having a life vest on a boat.

If you're considering refinancing, remember that the inclusion of a basement in your Georgia home can also impact insurance costs. Basements inherently possess a higher flood risk, which, in turn, can affect your policy's rate. Considering flood insurance as part of your refinancing calculations ensures you have a comprehensive understanding of future expenses:

|

Home Feature |

Influence on Flood Insurance Cost |

|

Elevation Relative to BFE |

Direct impact on premium rates |

|

Presence of Basement |

Increases perceived risk, may raise rates |

|

Policy Changes during Refinancing |

Opportunity to reassess coverage and costs |

Average Cost Range for Flood Insurance in AE Zones

As you delve into the financial specifics of flood insurance within Georgia's AE Zone, often termed a Special Flood Hazard Area, you'll find a range of rates that reflect the diverse landscape and risk profiles of these regions.

Comparable areas such as parts of Alabama and Virginia see average costs that can illuminate the broader spectrum of what you might expect to pay: premiums could extend anywhere from several hundred to a few thousand dollars annually, and your deductible – the amount you pay out of pocket before insurance kicks in – plays a pivotal role in these figures.

|

State |

AE Zone Premium Range |

Deductible Influence |

|

Georgia |

Variable based on risk assessment |

Significant in premium calculation |

|

Alabama |

Comparable rates offer perspective |

Choice of deductible affects costs |

|

Virginia |

Similar cost structures inform predictions |

Higher deductibles may lower premiums |

When taking out a loan for a property in such an area, lenders will often require flood insurance to protect the investment, which adds another dimension to your cost planning. Keep in mind, higher deductibles may reduce your insurance premium, but they also necessitate a greater financial reserve on your part in the event of a flood. Balancing those considerations with the rates that are typical for the AE Zone ensures you are prepared for both expected and unforeseen circumstances.

Understanding Your Property's Specific Risks

Your home in Georgia's AE Zone comes with its own set of hazards, and comprehending these risks is a cornerstone in selecting the right flood insurance. Just like homeowners in Connecticut or West Virginia might account for blizzards or mountainous terrain, you too must consider the flood risk specific to your locale. Choosing an insurance option that reflects the unique environmental challenges your property faces is vital.

An accurate estimation of your home's replacement value also plays a pivotal role amidst the calculations of flood insurance. It's not uncommon to wonder how this value is appraised in comparison to different states – whether it's the coastal properties in Connecticut or the rural homesteads of West Virginia. Ensuring your policy covers the full replacement value positions you to rebuild and recover should a flood occur.

Steps to Obtain an Accurate Insurance Quote

To secure an insurance quote that accurately reflects your exposure to flood risk in Georgia's AE Zone, first gather details about your home's specifics. For instance, a mobile home in Georgia may bear different insurance rates than one in Utah due to local environmental factors such as soil composition and typical rain patterns. Your quote will take these variances into account to provide a cost that mirrors your unique situation.

Next, reach out to a range of insurance providers to compare quotes. Just like the fluctuating waters of the Mississippi, insurance rates can ebb and flow based on a company's risk assessment and claims history in your area. Ensure that you disclose all relevant information about your property's risk profile to get the most accurate estimate.

|

Property Details |

Information Relevance |

|

Location and type of home (e.g., mobile home) |

Influences insurance rates by risk |

|

Local environmental factors (e.g., common rain patterns) |

Affects the accuracy of the insurance quote |

|

Insurance provider's risk assessment |

Varies between agencies, impacting premium costs |

HOW RISK RATING 2.0 AFFECTS AE ZONE RATES IN GEORGIA

As you explore the components that shape flood insurance premiums in Georgia's AE Zone, you'll encounter FEMA's newest methodology, Risk Rating 2.0.

This system has redefined how insurance rates are calculated, moving away from the simplistic binary of being in or out of a flood zone to a more nuanced approach. Now, factors such as your home's specific location, even down to the zip code, play a pivotal role. States like Louisiana, New Jersey, and even neighboring Tennessee are also navigating this shift, which has brought both clarity and complexity to estimating rates.

It's pivotal you grasp how this evolution from the old rate structures influences what you pay so you can anticipate and plan for these changes. Knowledge of your area's risk rating ensures you are not blindsided by adjustments to your flood insurance costs.

Introduction to FEMA's Risk Rating 2.0

Embarking on the path of understanding flood insurance costs in Georgia's AE Zone, you may have encountered FEMA's Risk Rating 2.0. This recent innovation reshapes the way real estate is assessed for flood risk, accounting for numerous factors including the exact location and the specific characteristics of your property: whether you're near a lake in Michigan or tucked away in the hills of Wisconsin, Risk Rating 2.0 calculates your premiums with precision.

|

Real Estate Location |

Risk Rating 2.0 Impact |

|

Near Michigan Lake |

Increased risk assessment |

|

Wisconsin Hills |

Variable risk depending on topography and water sources |

|

Georgia's AE Zone |

Premiums adjusted based on new rating methodology |

Grasping the details of Risk Rating 2.0 is key in anticipation of adjustments to your insurance premiums. This system provides a wealth of information, aiding you in making informed decisions about your flood insurance coverage and its associated costs, no matter the specifics of your locale.

Impact on Georgia's AE Zone Insurance Rates

The introduction of Risk Rating 2.0 by FEMA has had noticeable repercussions on the flood insurance market in Georgia's AE Zone. Unlike the system's one-size-fits-all approach, which could be likened to policies in states like North Carolina or California, this update calls for an expert assessment of individual property risks, affecting your investment in real time. Flood insurance now hinges on granular details, pushing for more personalized premiums.

Your role as a homeowner in this market adjusts accordingly; you're no longer comparing static rates, but rather navigating a fluid system where the expertise of your insurance agent shines. They'll need to factor in the geography peculiar to Georgia's AE Zone, much like assessing earthquake risks would be imperative in California. This ensures your investment is matched with an insurance policy tailored to the unique risks your property holds.

Comparing Old vs. New Rate Structures

Prior to the introduction of FEMA’s Risk Rating 2.0, flood insurance rates were based primarily on whether a property was inside or outside of a designated flood zone. This system didn’t account for specific nuances like potential storm surge or an area's plumbing infrastructure, elements that could dramatically affect the vulnerability of a property.

|

Rate Determining Factor |

Old Structure |

Risk Rating 2.0 |

|

Flood Zone Designation |

Primary Rate Indicator |

One of Multiple Factors |

|

Specific Risks |

Generally Not Considered |

Heavily Weighed |

|

Geographical Nuances |

Oversimplified Impact |

Detailed Assessment |

With Risk Rating 2.0, your flood insurance price is no longer a reflection of broad stroke assessments applicable to vast regions, akin to laws applied state-wide in Ohio. Instead, the cost of your flood insurance in Georgia's AE Zone now integrates a more precise review of your exact location within the floodplain and its susceptibility to flood risks such as storm surge and local plumbing weaknesses: nuances that define your property's unique flood profile.

How to Prepare for Potential Rate Changes

Preparing for potential rate changes brought by Risk Rating 2.0 means staying ahead of the curve, much like homeowners in Hawaii do by reinforcing structures against the threat of volcanoes. Factor in a percentage of your budget as a buffer for unexpected insurance increases, just as you would for natural disaster preparations in other states. This strategic planning allows you to navigate financial shifts without strain, mirroring the foresight seen in areas prone to wildfires or flooding.

While Georgia's AE Zone and Nebraska's plains may confront distinct issues, the method of keeping informed remains universal. Regularly review your policy details and stay informed about local and federal shifts in flood management—such knowledge aids in predicting rate fluctuations. Being proactive in your approach ensures that when changes come, they won't have the same devastating impact as an unforeseen natural disaster.

STRATEGIES TO LOWER FLOOD INSURANCE COSTS IN AE ZONES

As a Georgia homeowner situated in the AE Zone, you may feel the financial burden of flood insurance amplified by the ever-present threats of climate change.

From the unpredictable shifts seen in New Mexico's arid conditions to the historic floodwaters of Hurricane Harvey, the reality of escalating risks is undeniable. Fortunately, there are practical strategies to tackle high premiums. Initiatives such as flood mitigation measures not only boost your home’s defenses but can also lead to substantial savings on insurance costs. Procuring an elevation certificate—the homeowner’s equivalent of a performance review in Maryland's bayous or the rolling plains of North Dakota—can drastically alter your premium by confirming your home's relative safety.

Moreover, investigating the rewards available through the Community Rating System could lead to discounts reflecting your community’s collective efforts in flood preparedness.

As you weigh your options, navigating through various policy choices ensures that the cover provided aligns with your financial and protective needs, securing optimal savings in a landscape where proactivity is your greatest asset.

Implementing Flood Mitigation Measures

Proactive risk assessment and the application of flood mitigation measures may lead to lowered premiums, just as they do from the mountainous terrains of New Hampshire to the wide, open spaces of South Dakota. By carefully evaluating your home's vicinity to rivers and potential flood pathways, you can implement strategies such as constructing barriers or elevating your property to minimize risk—actions that South Carolina has embraced in its own flood-prone areas.

|

Action |

Impact on Premiums |

Examples |

|

Risk Assessment |

Potential for Discounted Rates |

New Hampshire's Terrain Evaluation |

|

Proximity to Rivers |

Adjustment of Premium Costs |

South Carolina's Flood Barrier Utilization |

|

Property Elevation |

Reduced Risk, Lower Premiums |

South Dakota's Elevated Homes |

Adopting measures that reduce the impact of flooding not only protects your property but also can result in more favorable insurance terms. The adoption of sensible landscaping to improve drainage, similar to practices in river-rich South Carolina, or retrofitting your home to prevent water intrusion as seen in South Dakota's resilient housing developments, are tangible steps that could positively sway the outcome of an insurance risk assessment and, consequently, your flood insurance costs.

Benefits of Elevation Certificates for Homeowners

Securing an elevation certificate may significantly influence your flood insurance premiums, mirroring Vermont's approach in its hilly landscapes. This document gauges your home's elevation in relation to the potential floodwaters, allowing you to qualify for more favorable insurance rates, much like residents benefit from in Alaska's diverse terrains.

For homeowners in Georgia's AE Zone, an elevation certificate can act as a lever to lower insurance costs, just as stringent building codes have done in Mexico's earthquake zones. By officially documenting the elevation data of your property, insurers in coastal Jersey, prone to flooding, or the floodplains of Missouri, reward proactive measures with reduced premiums:

|

State |

Elevation Certificate Impact |

Insurance Premium Outcome |

|

Vermont |

Documents elevation above floodplain |

May qualify for rate reductions |

|

Alaska |

Confirms compliance with flood regulations |

Supports insurance discount eligibility |

|

Mexico |

Assesses property against regional risks |

Facilitates adjustments in insurance costs |

|

New Jersey |

Essential for flood-prone coastal homes |

Can significantly lower premiums |

|

Missouri |

Shows elevation relative to rivers/streams |

Potentially decreases insurance rates |

Exploring Community Rating System Discounts

As you explore the Community Rating System (CRS), remember it's a methodology that could lead to discounts on your flood insurance premium, similar to how residents in Rhode Island have benefited. Your community's active engagement in floodplain management practices, measured by the CRS, can reduce the collective risk and, subsequently, the cost of insurance for homeowners like you.

In states like Nevada and Iowa, communities that exceed standard flood prevention requirements reap the rewards in the form of CRS discounts; a concept Pennsylvania has employed to incentivize mitigation efforts. Your proactive measures as part of your community's overall strategy can lead to reductions in flood insurance premiums, making this a valuable avenue to potentially alleviate the financial load of flood protection in Georgia's AE Zone:

|

State |

CRS Engagement Level |

Impact on Insurance Premium |

|

Rhode Island |

High implementation of CRS practices |

Eligible for significant discounts |

|

Nevada |

Commendable CRS participation |

Notable reduction in insurance rates |

|

Iowa |

Active in exceeding flood prevention standards |

Benefits from CRS-related premium discounts |

|

Pennsylvania |

Strategic CRS involvement |

Potential for substantial insurance cost savings |

Reviewing Policy Options for Optimal Savings

When perusing your policy choices, the utilization of data dedicated to flood management should inform your decisions. Drawing on lessons from states like Montana and Kentucky, where meticulous data analysis informs insurance premiums, ensures that you select a plan that aligns with specific regional risks and offers optimal savings.

Consider the insurance strategies employed by homeowners in Wyoming, where attention to detail in policy management can result in significant cost reductions. Your informed choice might involve seeking out custom coverage options that provide a balance of affordability and protection, unique to the landscapes of Wyoming itself.

THE ROLE OF PRIVATE FLOOD INSURANCE IN AE ZONES

While exploring your flood insurance options in Georgia's AE Zone, you might find yourself pondering whether to stick with the familiar National Flood Insurance Program (NFIP) or venture into the domain of private insurance. While residents in places like Kansas and Colorado frequently grapple with similar decisions, the distinctions between NFIP and private policies are pivotal.

Private insurers typically offer more flexibility and may present a viable alternative for properties in AE Zone, depending on individual circumstances. When assessing the suitability of private insurance for your home, consider the comprehensive coverage and potential cost savings they may offer, a strategy that has benefited homeowners from Arkansas to Illinois.

Beyond that, exploring private insurance could deliver advantages that align better with your needs than the federal offering – a revelation that homeowners even as far north as Minnesota have discovered. The right choice demands a keen understanding of both options and how they cater to the complexities of living in a high-risk flood area.

Differences Between NFIP and Private Insurance

When comparing the National Flood Insurance Program (NFIP) to private flood insurance, it's important to recognize that private policies may offer broader coverage options, especially regarding the gradual process of erosion. Private insurers might cover erosion-related damage if it’s a direct result of a specific peril, while the NFIP typically excludes coverage for erosion, viewing it as a non-sudden, ongoing event.

As you explore the differences, remember that private flood insurance can provide customized coverage levels, possibly extending beyond the maximum limits set by the NFIP. This means, if you're concerned about your property's susceptibility to erosion, a private policy may give you a sense of security that the NFIP can't guarantee due to its limitations on the types of covered damage.

Assessing Private Insurance Viability for AE Zone Properties

When evaluating whether private flood insurance is a suitable choice for your property in Georgia's AE Zone, consider the unique conditions of your home. Private insurers offer diversity in policy terms and conditions, meaning coverage can be more precisely aligned to the specific flood risks you face in Georgia's coastal or riverside locations.

Financial prudence dictates a thorough comparison of coverage limits and exclusions before deciding between private insurance and NFIP. The choice you make should ensure adequate protection without exceeding what you reasonably anticipate requiring in case of a flood event:

|

Policy Features |

NFIP |

Private Insurance |

|

Coverage Limits |

Maximum limits may not cover all expenses |

Potentially higher limits tailored to property value |

|

Exclusions |

May not cover gradual events like erosion |

Offers coverage that can include a wider range of damages |

|

Property Specificity |

Standard coverages with less flexibility |

Customizable policies to fit exact location risks |

As you analyze the viability of private insurers, pay special attention to their claim-handling reputation and financial stability. Your peace of mind comes from knowing that in the wake of a flood, your chosen insurer will provide timely and adequate compensation for covered damages to your property in the AE Zone.

Advantages of Private Insurance for Georgia Residents

Private insurance for Georgia residents in AE Zones can offer more personalized protection plans, tailored to address each homeowner's specific flood risk factors. Customizable limits and deductibles allow you to design a policy that not only meets your needs but also harmonizes with your financial strategy.

Considering private insurance might yield considerable benefits like shorter waiting periods post-purchase and more comprehensive coverage, giving you swifter protection when the waters rise. This can be particularly comforting when facing the unpredictable weather patterns and potential flood events Georgia is known to experience.

NAVIGATING FLOOD INSURANCE REQUIREMENTS IN GEORGIA

Securing your home in Georgia's AE Zone involves comprehending and meeting the mandatory insurance requirements that safeguard your property from flood risk. As you confront these necessitates, understanding the contrast between the lender-imposed coverage mandates and the thoroughness of a policy that offers ample protection is paramount.

Adequate coverage often exceeds the minimum terms set by financial institutions, providing an additional safety net for your investment. Moreover, ensuring all documentation is up to date and in full compliance is an indispensable step in maintaining a valid and beneficial flood insurance policy.

Navigating the stipulations set out by lenders and the additional measures one might take for comprehensive peace of mind therefore becomes a key consideration for homeowners in this high-risk flood area.

Mandatory Insurance Requirements for AE Zones

Living in Georgia's AE Zone puts your home in a high-risk area, and if you have a mortgage from a federally regulated lender, you are required to purchase flood insurance. This mandate is a safeguard, ensuring that both you and the lender have protection against losses due to flooding, which is not typically covered by standard homeowner's insurance.

To maintain compliance, your flood insurance coverage must equate to your home's rebuilding cost or be at least equal to the outstanding balance of your mortgage, whichever is lower. Staying vigilant about these requirements will help ensure you are never without essential coverage, particularly in an area as flood-prone as Georgia's AE Zone.

Lender's Insurance vs. Adequate Coverage Differences

As you secure a mortgage for a home in Georgia's AE Zone, understand that the lender will require flood insurance that at least matches the loan amount. However, this mandated coverage often falls short of providing full protection for your home, potentially leaving you underinsured in the event of a substantial flood incident.

It's crucial to assess the replacement cost of your home and gauge the adequacy of your coverage; not just to satisfy your lender, but to truly protect your investment. Often, the cost to rebuild can significantly surpass the outstanding mortgage, prompting the need for a more comprehensive policy that reflects the true value of your property.

|

Consideration |

Lender's Insurance Requirement |

Adequate Coverage Evaluation |

|

Coverage Base |

Outstanding loan amount |

Home's replacement cost |

|

Intended Purpose |

Protects lender's interest |

Protects homeowner's investment |

|

Financial Security |

May result in being underinsured |

Aims to provide full rebuilding costs |

Documentation and Compliance for Homeowners

Maintaining accurate and current documentation is essential for your compliance with flood insurance regulations. Keep your flood insurance policy, proof of premium payments, and any records of correspondence concerning flood insurance—such as an elevation certificate—in an organized and safe location for quick retrieval when needed.

Regularly review your policy and its requirements, ensuring your coverage reflects any changes to your property or the AE Zone guidelines. By staying proactive and informed, you solidify your home's defense against future flooding, while also keeping in step with both lender and federal flood insurance mandates.

FUTURE TRENDS IN FLOOD INSURANCE PRICING FOR GEORGIA'S AE ZONE

As you consider the long-term prospect of holding flood insurance in Georgia's AE Zone, you can't ignore the looming influence of climate change, legislative decisions, and evolving technology on your future rates. Fluctuations in the climate may drive more frequent and severe weather events, directly affecting how insurers calculate premiums.

On another front, lawmakers continue to draft policies that might alter the flood insurance landscape, potentially influencing what you pay to protect your home. Likewise, advances in technology are revolutionizing risk assessments, allowing for more precise mapping and predictive analytics.

Together, these factors could reshape the cost of your flood insurance, necessitating a vigilant eye on trends and a strategy adept at adapting to these pending changes.

Predicting the Impact of Climate Change on Rates

The escalating unpredictability of weather patterns due to climate change is poised to have a profound impact on flood insurance rates within Georgia's AE Zone. As severe weather events become more common, insurers are likely to adjust premiums to reflect the heightened risk of flood damage to your home.

You should anticipate the potential for increased insurance costs as advanced climate models and historical data trends drive insurers to reassess risk. Your proactive steps toward mitigation and adaptation today could help mitigate the impact of these rate adjustments tomorrow.

Legislative Changes and Insurance Cost Implications

Legislative developments can be significant game-changers in the flood insurance marketplace, particularly for homeowners in Georgia's AE flood zone. As laws evolve, they often bring reforms to the National Flood Insurance Program, which can lead to an increase or decrease in insurance rates, depending on the nature of the legislation: a relief in some cases but a strain in others.

Keeping abreast of new bills and amendments is key to forecasting the economic demands of insuring your property against floods. Understanding these legislative dynamics equips you to effectively plan for future insurance costs, maintaining financial stability as rules and regulations shift:

|

Legislative Change |

Potential Impact |

Homeowner Response |

|

NFIP Reformation |

Alters premium rates |

Evaluate coverage, adjust budget |

|

New Flood Insurance Bills |

May introduce new pricing models |

Stay informed, reassess policy |

|

Amendments to Existing Laws |

Could bring cost-saving opportunities |

Capitalize on potential discounts |

How Technology Is Shaping Insurance Premiums in AE Zones

Technological advancements are revolutionizing how insurers assess AE Zone properties, with precise satellite imagery and elevation data fine-tuning risk evaluations. As a homeowner, you may see your premiums reflect a more tailored approach to your specific location's risk profile, potentially leading to more accurate insurance pricing.

Furthermore, predictive modeling techniques, which incorporate climate projections and flood frequency data, are reshaping premium calculations. You'll benefit from insurers who now consider long-term risks more thoroughly, ensuring that your rates are aligned with the progressive understanding of flood probabilities in Georgia's AE Zone.

FREQUENTLY ASKED QUESTIONS

What factors influence flood insurance rates in Georgia's AE zones?

In Georgia's AE flood zones, insurance rates are shaped by factors such as home elevation, flood risk history, and building characteristics.

How has Risk Rating 2.0 changed flood insurance costs for homeowners?

Risk Rating 2.0 brings a more nuanced approach to assessing flood risk; instead of relying purely on flood zones, it considers individual property characteristics, which can affect insurance premiums for homeowners.

Can I reduce my flood insurance premium in an AE zone?

Absolutely, reducing your flood insurance premium in an AE zone, Georgia, is feasible by elevating your home, installing flood openings, and obtaining an Elevation Certificate for potential rate reductions. Consider these options to potentially lower your costs.

Is private flood insurance a viable option in AE flood zones?

Private flood insurance can indeed be a practical alternative for homeowners in AE flood zones, often offering broader coverage and potentially lower premiums than the National Flood Insurance Program.

What are the expected trends for AE zone flood insurance rates?

AE zone flood insurance rates in Georgia are anticipated to rise due to increasing flood risks and historical claim patterns, though individual premiums vary based on your property's elevation and mitigation measures.

CONCLUSION

Recognizing the intricacies of flood insurance costs within Georgia's AE Zone is crucial for homeowners to protect their property from flooding risks appropriately.

With factors such as your home's elevation and FEMA's Risk Rating 2.0 influencing premiums, staying informed enables homeowners to anticipate and plan for financial requirements effectively. Exploring both NFIP and private insurance options can lead to better-suited coverage and potential cost savings.

Ultimately, proactive understanding and preparation help homeowners navigate the dynamic flood insurance landscape, ensuring robust protection against unforeseen flood events.

Topics:

{kind=link}