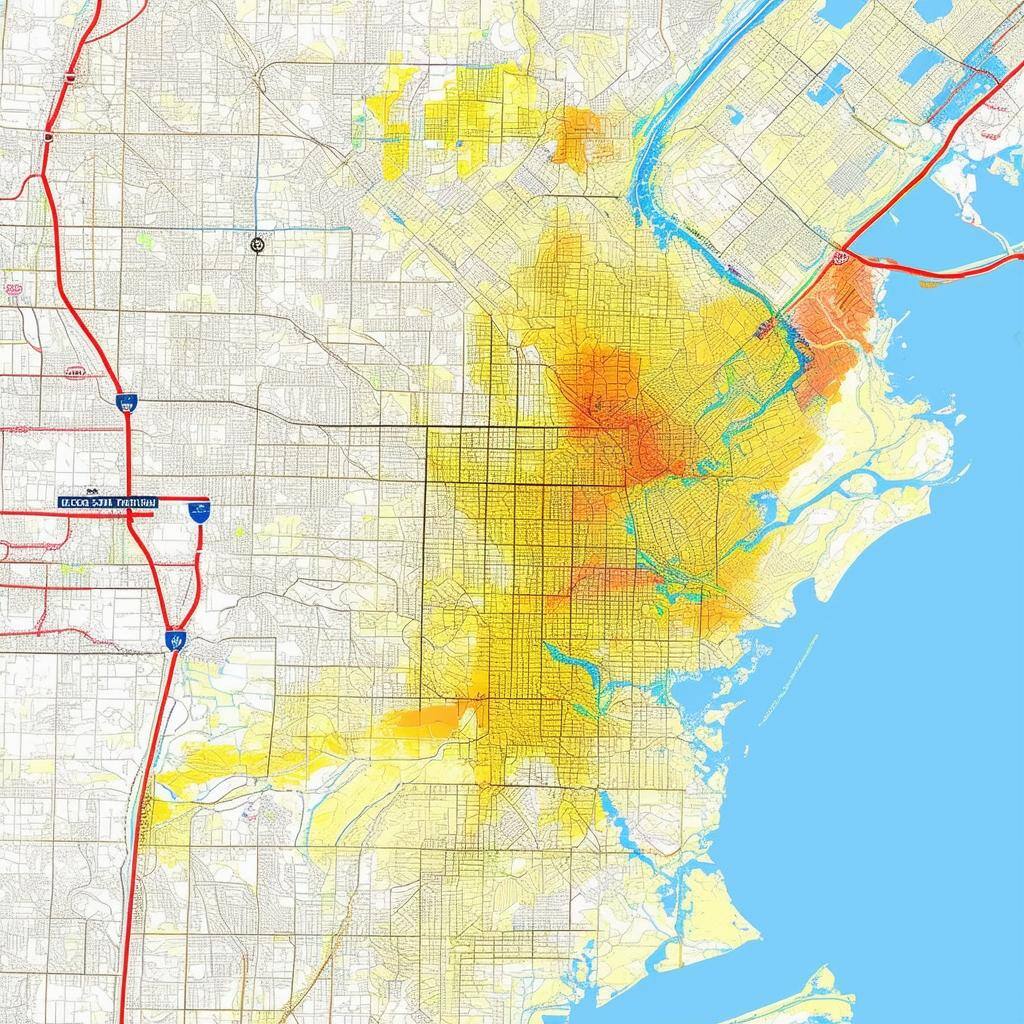

Key Changes in the Alabama Flood Zone Maps

Alabama's flood zone map updates highlight areas with increased storm hazards, particularly in regions vulnerable to Gulf storms. These changes significantly impact local communities by influencing property values, insurance requirements, and emergency preparedness protocols. Homeowners and property buyers should carefully review the latest designations, as being newly classified into a high-risk flood zone could result in:

-

Increased insurance premiums if properties are moved into high-risk zones.

-

New building regulations in flood-prone areas.

-

Adjustments to emergency management, as communities prioritize proactive flood risk mitigation

According to The Flood Insurance Guru, understanding these updates is essential not just for homeowners, but also for developers and real estate professionals. These flood zone changes directly affect insurance rates under the National Flood Insurance Program (NFIP) and can play a critical role in determining home values and future development plans.

Accessing the Updated Alabama Flood Zone Maps

For residents and property owners, accessing up-to-date flood map data is essential. Here’s how to navigate these resources:

-

AlabamaFlood.com: This interactive platform provides FEMA floodplain data by address or county. Homeowners can view FIRM, FIS, and other detailed tools such as Water Surface Elevations (WSELs) and depth grids. These resources help homeowners and developers better understand flood risks specific to their area.

-

FEMA Flood Map Service Center: Through FEMA's official portal, residents can view current and preliminary maps by searching their address. This site allows users to view and download effective and preliminary flood maps and access additional flood hazard products.

-

ADECA’s Interactive Floodplain Data: ADECA’s platform allows residents to view regulatory floodplain data statewide. This includes tools for understanding LOMR applications—vital for those whose properties have been affected by recent map changes.

-

Smart Home America: This organization specifically assists Baldwin and Mobile County residents in understanding new flood maps, interpreting map data, and navigating insurance needs. Smart Home America recommends obtaining an elevation certificate and exploring insurance options if properties fall within the 100-year floodplain.

How Recent Flood Zone Updates Impact Alabama Communities

Communities across Alabama are seeing the effects of these updates on local economies and insurance requirements. FEMA regularly revises flood maps as part of the National Flood Insurance Program (NFIP), making it critical for residents to understand new flood zone classifications. A reclassification into a high-risk zone can lead to:

-

Insurance premiums: Homeowners in Zones A and V face mandatory flood insurance, often with higher premiums than those in low-risk areas.

-

Property values: Homes located in high-risk flood zones may experience decreased market value due to increased insurance costs.

-

Building regulations: Stricter construction standards may apply, increasing the time and expense of development or renovations.

The Flood Insurance Guru emphasizes the importance of checking your flood risk regularly—especially in areas undergoing major development—so you can make informed decisions and avoid unexpected financial burdens.

Steps to Take if Your Property is Affected by Flood Zone Reclassification

If your property has been reclassified into a high-risk flood zone, there are a few steps you can take to protect your investment and potentially lower your insurance costs.

-

Verify Your Flood Zone Status: Start by visiting FEMA’s Flood Map Service Center, The Flood Insurance Guru's Flood Zone Tool, or Alabama Flood to confirm your flood zone status. This verification helps you understand any new insurance requirements or building regulations associated with your area.

-

Plan for Flood Mitigation: Evaluate your property for potential vulnerabilities. Simple steps like elevating key structures, improving drainage, or installing flood barriers can help reduce flood risk and may also lower insurance premiums. FEMA’s resources provide guidance on effective flood mitigation strategies.

-

Apply for Map Amendments or Revisions: If you believe your property has been incorrectly classified, consider applying for a Letter of Map Amendment (LOMA) or Letter of Map Revision (LOMR). This process requires survey data and possibly an elevation certificate to support your claim. The process, though administrative, can save on insurance costs if you successfully reclassify your property to a lower-risk zone.

Conclusion: Embrace Flood Preparedness and Protect Your Future

The updated flood maps in Alabama are a crucial tool for understanding your property’s flood risk. By staying informed, checking available resources, and proactively preparing for potential flooding, you can protect your home and investments. Accessing local resources, engaging in flood preparedness programs, and applying for map revisions if needed empowers you to navigate these updates confidently.

With these tools, FEMA resources, support from local authorities, and guidance from experts like The Flood Insurance Guru, you’ll be equipped to make well-informed decisions and build greater resilience against Alabama’s evolving flood risks.