In this podcast we are discussing three questions to ask before changing from the National Flood Insurance Program.

3 questions to ask

- Can you switch from the National Flood Insurance Program

- When can you switch from the National Flood Insurance Program

- Should you switch from the National Flood Insurance Program

.jpeg?width=242&name=download%20(8).jpeg)

Can You Switch

Switching from the National Flood Insurance Program may not be as easiest as you think it might be. Lets discuss four scenarios for witching

- No mortgage

- FHA mortgage

- Conventional mortgage

- USDA mortgage

- VA mortgage

.jpeg?width=271&name=download%20(5).jpeg)

So let's discuss if you don't have a mortgage. When it comes to flood insurance this is like breaking the handcuffs off. In so many situations mortgage companies control whether you can switch from the National Flood Insurance Program. By not having a mortgage you would have the opportunity to switch from the National Flood Insurance Program.

When it comes to FHA mortgages the handcuffs might be the tightest of any mortgage. FHA keeps their own guidelines and rules, as a result FHA mortgage customers are required to go through the National Flood Insurance.

Conventional, USDA, and VA mortgage customers don't have the handcuffs on as tight. These type of mortgage customers do have the ability to switch from the National Flood Insurance Program.

So now that we know which type of mortgage and non mortgage customers can switch from the National Flood Insurance Program let's discuss the timing.

When Can the Switch Happen

The National Flood Insurance Program has strict guidelines about when you can switch from their flood insurance program. Let's look at some history of how this has changed over the last year.

In the October 2018 bulletin FEMA stated that they would start allowing customers to switch to private companies before renewal. However about 6 months later they finally made a ruling reversing this decision.

So now FEMA follows the strict guideline of only allowing customers to switch from their flood insurance program at renewal. Waiting one day past the renewal date could lock you in for another 12 months.

So its important if you choose to make this switch that you make sure the new policy is effective at least the day before renewal.

We have talked about if you can switch and when can you switch from the National Flood Insurance Program. Now let's discuss should you switch from the National Flood Insurance Program.

Should You Make the Switch

So should you make the switch from the National Flood Insurance Program? Let's discuss three things that can help you with this decision.

- Coverages

- Premiums

- Claims

- Flood Maps

Coverages can be a big difference between the National Flood Insurance Program and the private flood insurance market. Some the differences are list below

National Flood Insurance Program

- Residential building coverage maxes out at $250,000

- Residential personal property coverages maxes out at $100,000

- No temporary living expenses

Private Flood Insurance

- Residential building coverage available up to $10 million

- Residential personal property available up to $1 million

- Temporary living expenses available

- Replacement cost on contents available

If you are looking for higher amounts of coverage or temporary living expenses then private flood insurance might be a good switch for you. Before making the decision lets review a few other things like premiums, claims, and flood maps.

When it comes to flood insurance premiums private flood insurance can sometimes be up to 50% less. However this is not always the situation. Generally in low risk areas or areas known as flood zone X the National Flood Insurance Program normally has the better rates. The National Flood Insurance Program also generally provides better rates in newly mapped areas.

So what are newly mapped areas? This are areas that may have recently been reclassified from low risk zones to high risk zones. The National Flood Insurance Program gives a newly mapped rate for the first 12 months while private flood insurance does not.

So let's discuss one of the most important things when it comes to flood insurance. How do flood insurance claims impact the ability to make the switch from the National Flood Insurance Program.

Claims can have a big impact on the ability to switch from the National Flood Insurance Program. One reason is they treat claims differently.

For example if you have had one claim of $50,000 or more then it might cause you to be ineligible for most private flood insurance. However the National Flood Insurance Program will not decline you because of claims.

Private flood insurance may also put moratoriums on new policies in areas that have had a high amounts of claims. This happened in Houston Texas after hurricane Harvey limiting most flood insurance options to just the National Flood Insurance Program.

Now let's discuss how flood maps can impact the ability to make this switch.

Flood maps with the National Flood Insurance Program have been outdated for a long time. FEMA tries to update these maps but there are some areas in Kansas and Missouri that haven't seen flood map updates in 50 years. The technology that the National Flood Insurance Program uses does not address the true risk in many situations.

One example is many parts of Houston Texas that were zones for low risk but quickly flooded during hurricane Harvey. Private flood insurance companies use alot of different technologies that focus on the structure on a property and the entire property.

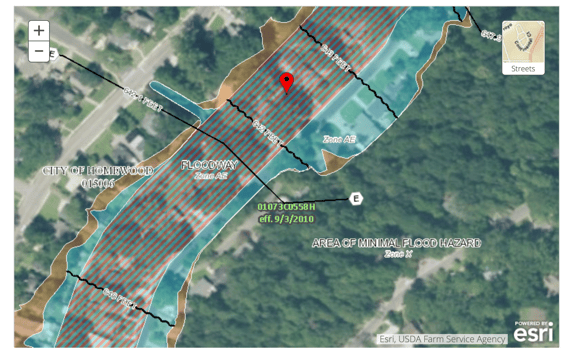

Another issue with these flood maps are the flood ways. These are the overflow areas along creeks, streams, and rivers. The National Flood Insurance Program does not charge more or reject property owners because they are located in this area. However many private flood insurance companies will reject someone if they are located in a floodway and others will charge much higher premiums.

So as you can see making the switch from the National Flood Insurance Program should not be a quick decision. There are a lot of different factors that should be considered. If you have questions about making this switch or if this switch is good for you click the link below to contact us. You can also visit our YouTube channel or Facebook page where we do daily flood education videos. Remember we have an educational background in flood mitigation so we are here to help you understand flood risks, flood insurance, and mitigating your property.

{kind=link}