It's cool to know how utilities and appliances impact your flood insurance!

In today's episode we cover how your household or business utilities and appliances affect your flood insurance. We'll cover on how the placement of appliances like an air conditioner will impact your flood insurance.

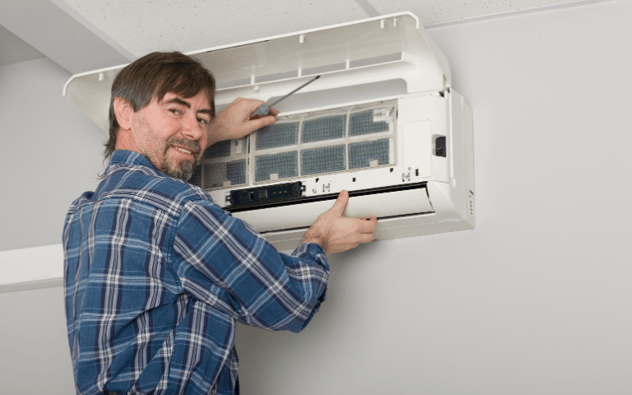

As you'll see in this video, the air conditioner is lifted a little bit off the ground. It basically is in the lawn of this homeowner. In my experience, I've seen properties that has appliances like water heaters, window air conditioner or any air conditioning equipment, and I wonder if these homeowners are aware of the impact of such appliances to their flood insurance.

Flood insurance policies are closely looked into by insurance companies since it has a different set of standards when it comes to flood insurance requirements. These standards and guidelines are set by the federal government and federal flood insurance through the Federal Emergency Management Agency (FEMA) and the National Flood Insurance Program (NFIP) to determine the flood risk and its respective flood insurance coverage and premium for an insured building. Remember, your homeowners insurance policy is separate from your flood insurance.

See, when you have appliances or utilities, like maybe a space heater, which sits below the base-flood elevation, you're going to have to write it as your lowest rated floor. This includes your garage or swimming pools since they're considered as a separate part of your property when in comes to any flood insurance policy. This is basically because these things will be impacted by flood damage regardless despite being considered under the contents coverage. I mean, I've seen swimming pools get totaled by massive flood water damage.

It's important to remember that if you have a floor that's below the base-flood elevation, it will increase your flood insurance rates and can financially hurt in 2 to 3 years. This can also be a reason why you're going to have a difficult time removing your property from being in a high-risk flood zone.

For a better example, say you have a basement under construction without anything in it except a space heater and an air conditioner. This floor will have to be written as your lowest rated floor. If you remove it, then you might get this off your mind altogether.

The same goes for any utilities or appliances that is outside the house and sits comfortably above ground. Say, your house structure is above the base-flood elevation, but you have an AC that sits below the base-flood elevation then it's going to be one big hurdle if you want to change your flood zone. If a utility or appliance sits below the base-flood elevation, it will still be considered as the lowest rated floor of the entire property.

The only workaround is to have the utility item or appliance be lifted or moved up 6-inches or whatever the distance is needed for it to be above the base-flood elevation.

So, if you have questions on flood insurance, your flood insurance rating, and how to really look into your flood insurance rating with all your goodies like these included, please feel free to contact us and consider subscribing, dropping by, and watching our educational flood videos over at YouTube.

Remember, we have an educational background on flood mitigation and we want to share this flood education and awareness to you, so that you too can get prepared for when crap, like having higher rates due to appliances below the base-flood elevation, happens and more.

Topics:

{kind=link}