The Federal Emergency Management Agency (FEMA) is rolling out changes when it comes to flood insurance rates across all states in the country. Today, we will unpack these changes coming to Texas and how they can impact your flood insurance in the future.

Texas has been one of the hot topics when it comes to flood insurance. Other than its overall geographical setup where most of the communities sit on low-lying areas, a lot of things are changing with the Texas Disclosure Law and the upcoming Risk Rating 2.0 from the National Flood Insurance Program (NFIP) and FEMA. The state also had also faced a lot of flood threats in the past few months. As the spring season entered the country, Texas also faced a lot of threats of hailstorms and flash floods.

Getting a flood insurance policy is a great start in making sure that you're protected and prepared from the possible flood damage that this type of disaster can cause. However, this won't really get you far if you're out of the loop when it comes to the changes that will happen with it. This involves where flood insurance policies are available, flood insurance options through the federal government or private flood insurance companies, the methodology of how your flood insurance premium is calculated, and things like that.

We want to help you unpack the changes with this update and how it will impact flood insurance for Texans moving forward. The Risk Rating 2.0 is expected to drop on October 1st, 2021.

The NFIP 2.0

The Risk Rating 2.0, or commonly known as NFIP 2.0 as well, is more of a move of equity. This update on the federal flood insurance program itself will allow you to no longer pay more than your fair share when it comes to premiums as this would now be based on the value of your property or home starting this October.

It's important to keep in mind however that this doesn't mean that all homeowners with an expensive property or high-valued homes will be getting rate increases or premium increases with FEMA or lower-valued homes in Texas will be sure to get a decrease. There's a lengthy period of time in which both FEMA and private insurance companies work in making sure that you receive accurate numbers on the cost of flood insurance for your property. These things are as follows:

- Overall flood risks and flood frequencies in communities

- History of flood damage and flood loss

- History and number of flood insurance claims or flood claims made in the last ten years

- Mitigation efforts on the listed structure. Does the property have flood openings? Is the lowest floor above the base flood elevation?

- Flood Insurance Rate Maps designation. Where does the property sit in the flood maps? Are you in a high-risk flood zone or a low-risk flood zone?

These are just to name a few when it comes to flood insurance rating and flood insurance prices across all carriers. You also want to consider these things since it's best to have a great understanding of the actual risk that your property might face.

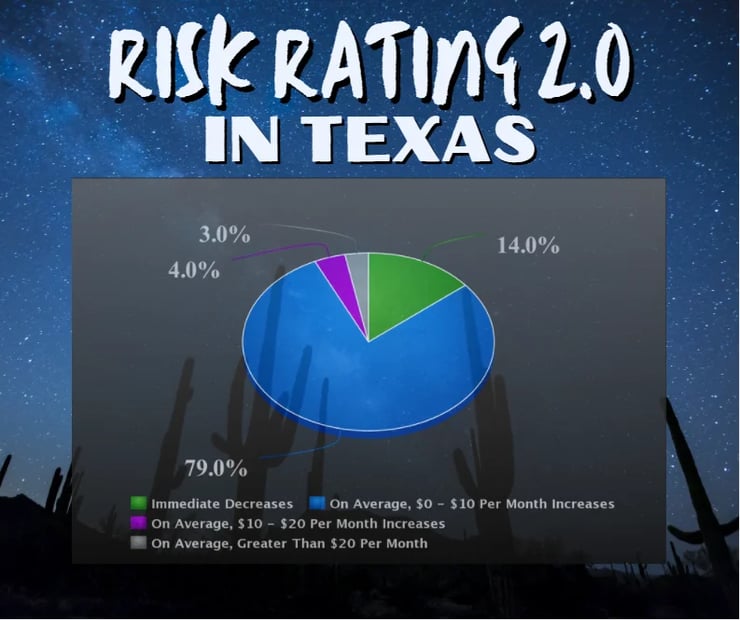

When it comes to the rate changes happening across the country, you're going to see these colors in ranges which represent these changes with flood insurance rates from FEMA. Now, each of these colors represents the good, the bad, and the ugly changes coming to each state.

The Good

Let's start off with this Risk Rating 2.0 train with the good things coming to federal flood insurance. We'll have this shown as the green portion of the graph you'll see below.

This will impact about 14% or 106,729 policies that FEMA has in force in the state. The good thing about this is that generally, this indicates that you're going to get a decrease in your flood insurance rates with FEMA once the Risk Rating 2.0 kicks in.

The decrease will be up to more than $100 (>$1200 per year) and can take effect immediately once you adopt the new rating system from the NFIP 2.0. Considering that this affects more than people in the hundred thousand, this can really help a lot of those who are being moved into a high-risk flood zone, paying for expensive premiums previously, or new to the NFIP.

The Bad

Now, let's move into the blue portions which take up most of the population of the policyholders in the state: the bad change.

This will impact a whopping 79% or 607,645 policies in Texas. This means that most of the policies in the state will have to go through this bad change which will be in form of a small increase in federal flood insurance rates.

The increase will range from $0 to $10 per month ($0 - $120 per year). This means that you might not even a change in your flood insurance rates and will have to stick with whatever amount you're paying right now even when the Risk Rating 2.0 kicks in (the $0 per month).

The Ugly

Finally, let's discuss the percentage left with these new rates from the NFIP 2.0: the pink and grey portions. These two will still get you an increase however let's put a disclaimer immediately how the grey portion will be the uglier change between the two. Let's dive down to better know these two.

The pink portion will impact 4% or 32,660 policies in the state. If you're part of this, you'll be getting an increase on your flood insurance rates ranging from $10 and up to $20 per month ($120 - $240 per year).

The grey portion, which covers the smallest amount, with only 3% or 21,525 policies to be impacted by this change. This time around, the increase will be drastically different from the pink portion since the increase will be more than $20 per month (>$240 per year). You may even start to get an increase of more than $100 per month (>$1200 per year) on your flood insurance rates depending on various factors in determining your rate with FEMA.

You can see the full graph of these changes below:

When Will It Happen?

Now, the date when you can adopt this program really depends if you're doing a renewal or if it's a new business policy. You see, you can expect these changes to start on October 1st and you're going to adapt to these rate changes if you're buying flood insurance from FEMA on or after that date.

On the other hand, if you're doing a renewal with FEMA after that date then you don't have to take in these new rate changes until April 1st, 2022.

So, you want to be very ready for this. We've been talking about this since last year since basically the NFIP is already 30 years old already and is in need of this change. Some would even say that the current NFIP ways are already outdated which really begs for this Risk Rating 2.0 to happen.

If you have questions on these upcoming changes, what are your flood insurance options in Texas, or anything about flood, reach out to us through the links below. You can also watch this on our YouTube channel.

Remember, we have an educational background in flood mitigation and we want to help you understand flood risks through education and awareness in flood insurance and preparedness.

{kind=link}