This is no April Fool's joke, but a big change is coming to the claims process and rating for federal flood insurance.

In this article, we want to discuss the changes to the claims variable and how your flood insurance premiums are going to be impacted by the new claims rating system with the Federal Emergency Management Agency (FEMA) and the National Flood Insurance Program (NFIP). We want to discuss three (3) things that you to know about this upcoming change to flood insurance on April 1st, 2023.

Flood Insurance Claims

First, let's cover how flood insurance claims can impact not only your flood insurance policy but also how risks are viewed for your property or home.

When it comes to the federal side of flood insurance under the National Flood Insurance Program (NFIP), flood claims can directly impact your rates. This happens in two forms with Risk Rating 2.0: the Severe Repetitive Loss (SRL) and the Claims Variable. As a policyholder, it's important to keep in mind these keywords.

The Severe Repetitive Loss (SRL) list for properties indicates that the property has filed more than one flood claim in a 10-year period. Generally, this indicates a higher risk for flooding and will in turn impact the flood insurance premiums of a certain policy.

The claims variable on the other hand is the newer claims rating factor that was introduced with Risk Rating 2.0. Initially, this new system will clean the policyholder's flood claim history and start from scratch.

However, if a claim is filed and paid out, the policyholder will see a potential increase in premium rates as FEMA will conduct a 20-year lookback where they will count all of the flood claims made during that period. This claim variable will produce a number that becomes a multiplier for the rates and is dependent on the number of claims made during that period.

But what are the coming changes to claims with FEMA for April 1st, 2023?

3 THINGS CHANGING WITH CLAIMS

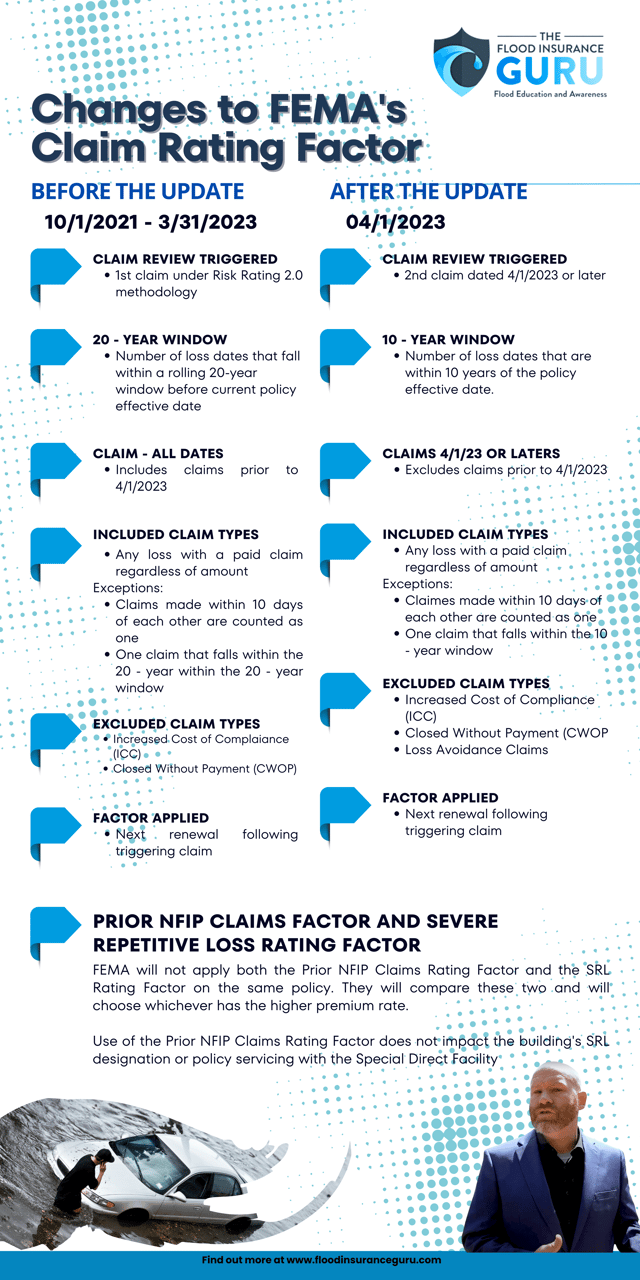

1. 10-YEAR WINDOW & CLAIM DATES

One of the big things to have changed when it comes to federal flood insurance claims rating factor is dates.

Previously, if you were to file a claim under Risk Rating 2.0 with FEMA, they will start to do a 20-year lookback which means that they will look at all the claims made on the property for flood insurance for the past 20 years. The number of claims made will be used as a claim variable which acts as a multiplier for your flood insurance rates.

This lookback is changed to only do a look back for 10 years only. This can make it easier for property owners to avoid a higher claim variable.

Another change that involves dates is more focused on when FEMA's claim rating factor kicks in. Previously, any and all claims made during Risk Rating 2.0 will immediately trigger the claim review. These claims may be from any time prior to April 1st, 2023.

Basically, all of the claims made in the past 20 years regardless of the date will be sent as part of the review. Generally, this could also mean that there will be higher rates due to having a higher claim variable.

For this new update, you will have to file a claim on April 1st, 2023, or later for the claim review triggered. This simply gives more leniency and a chance for property owners to get more breathing space before claims impact their rates.

This is important because...

2. WHAT TRIGGERS THE CLAIM REVIEW

Before this upcoming update, even if you file just a single claim during Risk Rating 2.0 — which means any flood insurance claims made before April 1st, 2023 — will immediately trigger the review. This can really hurt especially with how flooding behavior has changed in the past decade.

With this update, you will now have to file 2 claims within this 10-year period for the claim review to be triggered.

We recently had a customer who had these troubles with the previous system where they had two flood claims made in the last 20 years but only one in the last ten years. In the Risk Rating 2.0 claim review, this meant that both claims will be part of the claims variable however with this update, only one of them will be considered.

3. WHAT CLAIMS ARE EXCLUDED

Let's move into another category in this update which concerns more about what types of claims are excluded in the Risk Rating 2.0 review and which ones are excluded in this April 1st, 2023 update.

Previously, the only exclusions are for Increased Cost of Compliance (ICC) and Closed Without Payment (CWP). So this meant that if you filed a Loss Avoidance Claim, you will see this included. Generally, this meant that the previous system also uses Loss Avoidance Claims to trigger the claim review.

With this new update, Loss Avoidance Claims will be added to the exclusions. These are claims made for helping your property avoid damage from flooding which includes things like sandbagging, and creating temporary levees, or water pumps to name a few. Generally, this goes around for $1,000 with a standard flood insurance policy.

So you can imagine that if these are still to be included with the rating factor for claims, it could really become a burden for policyholders, but that won't be the case anymore.

You can see the full breakdown of what we discussed here:

These are the upcoming changes to how flood insurance claims work with federal flood insurance. If you are ready to take the next steps to get the right flood insurance coverage then there are three simple steps.

- Fill out this form —

- Talk with our flood education specialist.

- Get back to the important things in your life.

Got more flood insurance questions? Visit our Flood Learning Center below to know more:

Topics:

{kind=link}