As we welcome the new year of 2023, we also welcome the changing flood industry. One of these changes coming this month is for flood insurance rate maps (FIRM) or simply known as flood maps.

In this blog, we talk about why it's important to know the changes to the communities in Kaufman County, the flood hazard determinations with these new maps, and the good, bad, and ugly changes that this new flood map may bring to residents of Kaufman County in Texas.

Texas and Floods

Texas is no stranger to floods. If we look back to 2022, we can easily see this ring true as areas like Dallas-Fort Worth experienced one of the deadliest floodings in the state. This was caused by continuous heavy rain that dumped around 15 inches of rain in the area which started on August 21st.

Dallas firefighters responded to 195 high-water incidents across the city of Dallas with 39 rescues being carried out. On the other hand, Fort Worth firefighters responded to 174 rescues and other high-water incidents. All of these in just mere 24 hours.

Kaufman County, on the other hand, had a similar experience in May of 2022 although not in the same severity. This is when drenching rain flooded Kaufman Co. which caused South Washington Street to be closed temporarily.

As one of the fastest-growing counties in Texas, seeing an 18% boost in population between 2019 and 2021, it's important to be aware of how these events could impact the area and how it changes flood risks for residents.

So, let's talk about the new flood maps coming to Kaufman Co. and what it means for your flood insurance moving forward. It's important to note that these reports coming from the Federal Emergency Management Agency (FEMA) will be based on their flood insurance study.

The Good

Let's start off with the good things that we're seeing with this new flood map. We're seeing around 60 properties that will be experiencing an "in to out" movement.

This means that there are around 60 properties that are currently mapped into the special flood hazard areas (SFHA) and they are getting mapped out of it. In simpler terms, this could also mean that these properties are moving out of a high-risk flood zone or some would call this moving into flood zone X.

Now, why is this a good thing? For one, this means that mandatory flood insurance purchases will no longer be required for these properties as low-risk flood zones like flood zone X aren't required to have flood insurance with the property.

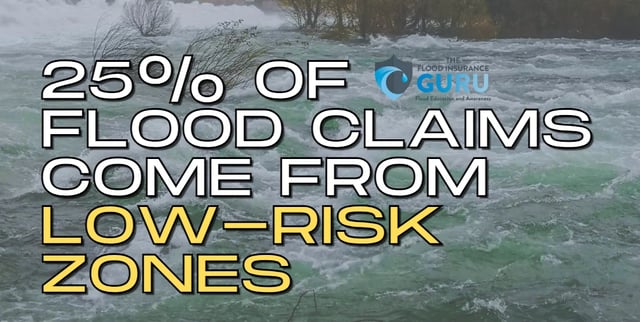

Although flood zones no longer impact flood insurance costs especially when it comes to premium rates, you should still have a flood policy ready to cover you from flood damage even if you're in a low-risk zone. This is important to remember especially since at least 25% of flood claims with FEMA come from these low-risk areas.

Simply put, even low-risk flood zones like flood zone X will still get flooded at some point in time or given the right conditions.

The Bad

Now, let's move to the bad changes which are indicated by an "out to in" movement. As the direct opposite of the good, this means that we're looking at properties that are going to be moved into a high-risk flood zone when originally they were in a low-risk flood zone. Some would call this "moving into a flood zone" or being mapped into flood zone A.

According to FEMA's new flood map, only 12 properties will be experiencing this movement. This also means that if you experience this out to in movement, you'll be required by the state and your mortgage or bank to get a flood insurance policy with the property as it's moved to a special flood hazard area (SFHA).

Historically, this type of change can mean that you will see an increase in your flood insurance risk and an increase in your premium rates. This is because, with National Flood Insurance Program (NFIP) before, flood zones are one of the main basis for premium rates.

The Ugly

Lastly, we have the "in to in" movement. This generally indicates that a property that's already in the SFHA will be moved deeper into it. This could mean that you're currently in flood zone A and now you're being moved into flood zone AE. This is expected to impact 1830 properties in Kaufman County when the flood map of January 12th kicks in.

This movement generally also indicates an increase in your risk of flooding the property. This can also mean that you may see some stricter flood insurance requirements and a change in your overall flood risk as well.

How To Fight Flood Map Changes

Changing Your Flood Zone

Let's just say you have a property that's mapped into a low-risk flood zone like flood zone X, this doesn't mean that that building will stay in that zone forever. This is especially true as flooding impacts how flood insurance rate maps (FIRM) work.

Sometimes, when a flood insurance rate map update comes to your community, this could mean that you might see your property get moved into a high-risk area like flood zone A or flood zone AE. Having your property or building mapped into a high-risk flood area generally results in a mandatory purchase of flood insurance.

To see your revisions to your community's flood maps, you can CLICK HERE to visit the official website for FEMA flood insurance rate map (FIRM) changes.

This requirement might come from your mortgage lender or the state law itself such as the Federal Emergency Management Agency's (FEMA) standards. But, what if you know that your property shouldn't be in a high-risk flood zone? How do you fight these changes?

This is where what's called a Letter Of Map Amendment (LOMA) comes in to save the day.

Letter Of Map Amendment

A Letter of Map Amendment (LOMA) is an official document that's issued by FEMA to process the change of a flood zone designation for a property.

An elevation certificate will show a more accurate representation of your property such as its risks from flood water, base flood elevation, its exact distance from your lowest habitational floor, and other relevant information. A LOMA is achieved after a successful application for a Letter of Map Change (LOMC) thru FEMA's official website.

It helps to have the necessary information and documents when applying for a LOMA. One of the helpful supporting documents you can provide is an elevation certification.

Although elevation certificates are no longer required — especially with the recent update to the National Flood Insurance Program (NFIP) and Risk Rating 2.0 — this can really help a lot in proving the validity of your request to be mapped out of a high-risk area.

Flood REMINDER

So these are the good, the bad, and the ugly changes coming to Kaufman Co. When it comes to actual flood risks, the reality is that even low-risk flood zones can be flooded too. This also means that getting a Letter of Map Amendment (LOMA) done won't guarantee that your home no longer has flood risks.

This is why we still encourage property owners to get flood insurance coverage for their property. A single flood policy will be able to provide building and contents coverage, so both the structure and your personal property inside it will have flood protection.

If you have questions regarding flood zones, flood insurance, or anything flood-related, click below to access our Flood Learning Center to get your answers.

Ready to start simplifying your flood insurance? Just follow these three simple steps:

- Fill out this form —

- Talk with our flood education specialist.

- Get back to the important things in your life.

Topics:

{kind=link}